A Portrait of Warren Buffett — The Earlier Years

I’ve had it so good in this world, you know. The odds were fifty-to-one against me being born in the United States in 1930. I won the lottery the day I emerged from the womb by being in the United States instead of some other country where my chances would have been way different.

Warren Buffett about winning the “Ovarian Lottery,” 2004

Cash combined with courage in a crisis is priceless.

Warren Buffett after the attacks on 9/11/2001

From time to time in our quarterly investment commentaries, we like to recount stories of exceptional investors. Most of us have an interest in creating wealth for ourselves and for our families, and studying the lives and the investment methods of hugely successful investors can not only be compelling reading but also prove highly instructive. And who better to study than Warren Buffett, who announced at the Berkshire Hathaway Annual Meeting last May that he will be retiring at the age of 95 at the end of this year? As chronicled in Roger Lowenstein’s Buffett: The Making of an American Capitalist, $10,000 invested with Buffett in 1956 translated into $80 million by 1994. By the end of 2024, the number would have increased to $2.4 billion! Little doubt that Buffett is the greatest investor of all time!

Starting with no capital other than the money he earned in his teens as described below, Warren Buffett’s current net worth is approximately $145 billion. The enormous wealth that he has created is in addition to the $60 billion that he has already donated to various foundations and charitable causes. And Buffett built this huge fortune through using his wits — through his discipline, his understanding of intrinsic value, his ability to gauge risk, his courage in taking bold moves in the stock market, and his understanding of people. Unlike most of the world’s richest people, he did not accumulate his wealth through the creation of companies that produce goods or services but through compounding his capital over more than seven decades.

Many barrels of ink have been spilled chronicling the remarkable life of Warren Buffett. And, over the past several decades, his every investment has been in the news, and his folk wisdom, detailed in his legendary Annual Reports, has been dissected and minutely analyzed by many. So, instead of depicting the trajectory of Buffett’s life in the 21st century, this commentary focuses on Buffett’s earlier years — his upbringing, his difficult childhood, his schemes to earn money as a youth, his family life, his investments before the age of 40, and how his original investment methods morphed into his more recent investment approach.

One of the best biographies of the “Oracle of Omaha” is The Snowball: Warren Buffett and the Business of Life written by Alice Schroeder, published in 2007. Before writing Snowball, Schroeder worked first as a CPA and later as an insurance research analyst for a number of investment firms including Dowling Partners in Hartford, CT. In writing this biography, she spent over 2,000 hours with Buffett

and interviewed 250 people. Snowball is an outstanding 700-page biography dealing not only with his investment successes and occasional mistakes, but also offering an intimate portrait of the man, “warts and all.” Much of this commentary is based on Snowball and is intended for those who would like to know about the man and his investment methods but do not have the time or inclination to read Schroeder’s excellent book. Another source for this essay is Buffett’s Early Investments — an excellent book by Brett Gardner about Buffett’s investment successes and failures from 1951 until 1969. From 1951-1956, Buffett was investing in a 50-50 partnership with his father, and then in 1956, he began a series of partnerships with friends and family members, called Buffett Associates, Ltd. Ultimately in 1962 these partnerships were merged into his famous partnership, Buffett Partnership Ltd. In 1969, with the market too richly valued for his taste, Buffett dissolved this partnership, and all his investments were made thereafter through Berkshire Hathaway. Our interest in this commentary focuses primarily on his early years, when his investment returns were nothing short of spectacular, rather than on his later higher-profile investments, as these have been well covered and well-documented in many publications.

Childhood (1930-1936)

Born in Omaha in the early years of the Great Depression, Warren Buffett was the son of Howard and Leila Buffett. The first Buffetts came to Omaha in 1867. Buffett’s grandfather, Ernest, ran a grocery store. He and his wife, Henrietta, had five children — four sons and a daughter — all of whom graduated from the University of Nebraska. Howard, the third son and Warren’s father, became a stockbroker and put out his shingle in 1932 when the Great Depression was at its worst. He married Leila Stahl, whom he had met when they were students at the University of Nebraska; both worked at the college newspaper. Warren’s older sister, Doris, was born in 1925; Warren arrived five years later; and his younger sister, Bertie, was born in 1933. Their mother, Leila, appeared outwardly to be the perfect mother and wife — dutiful, motherly, and upbeat. But when Doris and Warren were toddlers, Leila would frequently explode in rage at something that one of them had done. She would often berate the children for an hour, ceasing only when both Doris and Warren were weeping helplessly. These tirades almost surely contributed to Warren’s insecurities later in life.

From his earliest years, Warren was obsessed with numbers. At the age of six and seven, he already liked anything that involved counting, collecting, and memorizing numbers. He loved to read and was very competitive. He was good with adults in his early years but awkward with his peers – especially girls.

Accumulating Capital (1936-1947)

Warren Buffett earned his first few cents selling packs of chewing gum, buying a pack of gum for five cents and selling it for seven cents. If someone wanted to buy only one stick of gum, Warren stuck to his guns and never broke a pack. These pennies were the first snowflakes in the big snowball of the future. Next was selling cans of Coca-Cola. He bought cartons of Coke and went house to house on summer nights selling individual bottles of Coke. For every six bottles, he earned five cents. At the age of six, he had his own bank account where the pennies and nickels began to mount. By the time he was nine or ten, he and a friend were selling used golf balls which they found at a nearby golf course. At age ten, he got a job selling peanuts and popcorn at the University of Omaha football games. Soon, he began to read books about the stock market and was thrilled to “mark the board,” chalking stock prices on Saturday mornings (in those days the stock market was open for several hours on Saturday).

At age 10 in 1940, Buffett was taken on a trip to New York City by his father. Above all, Buffett wanted to visit the New York Stock Exchange. On the trip, Buffett briefly met Sidney Weinberg, senior partner at Goldman Sachs, an immigrant’s son who had worked his way up the ladder, starting as a porter’s assistant emptying cuspidors. Buffett never forgot his brief encounter with Weinberg, who asked him: “What stock do you like, Warren?” His visit to Wall Street planted a vision of his future. He wanted to be wealthy. He wanted to be independent and work for himself, and money could make that happen. Back in Omaha, Buffett found a book in the library entitled One Thousand Ways to Make $1,000. In other words, a total of one million dollars. The book taught him about the magic of compounding. He realized that if he started building his capital now and it compounded at 10% or more annually, one million dollars could be achieved by the age of 35. That became his vision. In his mind, he pictured a snowball growing as it was rolled across the lawn — a gigantic snowball.

In 1942, at the age of 12, Buffett’s hoard of savings amounted to $120. It was then that he bought his first stock: he and his sister, Doris, pooled their money and bought 3 shares of Cities Service Preferred at $38.25 a share. Shortly thereafter, the stock dropped 29%. His sister reminded him every day on the way to school about the stock’s decline. When the stock recovered to $40 a share, he sold it, to his great relief. Soon thereafter, the stock soared to $200 a share. This taught Buffett several lessons, and he called this episode one of the most important in his life. He learned first not to overly fixate on the cost of the stock, and secondly not to rush in unthinkingly to grab a small profit. Finally, this episode taught him to be careful about investing other people’s money; he knew that he would need to succeed before accepting that responsibility.

In 1942, Warren’s father, Howard, ran for Congress as a conservative Republican and was elected. The family moved to Washington, D.C., where Warren had a difficult time fitting in at school. He was a year younger than most in his class, and he was very socially inept. Buffett was miserable for a few years, and he and a friend even ran away, making it all the way to Hershey, PA before being grabbed by the police who were looking for them. Ultimately, it was his work ethic that saved him. He became a paperboy and landed a huge contract for a toney apartment complex, The Winchester. At the age of 14, he filed his first income tax return. By that time, he had saved $1,000 — over $18,000 in today’s dollars. A year later, Buffett had saved $2,000, and he bought a 40-acre farm in Nebraska for $1,200. A tenant farmer worked the land, and they shared the profits.

At the age of 15, Buffett was a very insecure teenager. During his teen years, he read biographies of great entrepreneurs like Vanderbilt, Rockefeller, and Carnegie. He was terrified of public speaking but then read and was greatly influenced by Dale Carnegie’s famous book, How to Win Friends and Influence People. He began to follow the rules Carnegie set out. Unlike most people who read Carnegie’s book and promptly forgot the rules, Buffett practiced them assiduously. And in high school, he found they worked. All the while he was finding new ways to earn money. Perhaps the most ingenious way that Warren and a friend found to make money was buying used pinball machines, refurbishing them, and placing them in barbershops around Washington. They split the proceeds with the barbershop owners and raked in the money. Soon Buffett’s stash was up to $5,000.

In 1947, Buffett graduated from high school 16th in a class of 350 and was accepted at the University of Pennsylvania. He didn’t really fit in; as one friend said, “He seemed an odd mix of immature kid and brilliant prodigy.” He liked individual sports like ping-pong and golf but never really enjoyed team sports. He had only one date during his two years at Penn. In the 1948 congressional elections, his father was defeated, and the family returned to Omaha. Buffett decided to finish his last two years of college at the University of Nebraska, graduating at the age of 20. Fixing his sights on Harvard Business School, he traveled to Chicago for his interview, which did not go well. Buffett later called his rejection by Harvard “the pivotal episode in his life.” Researching other business schools, he came across Benjamin Graham and David Dodd, who were at Columbia University. He recognized them as he had just read Graham’s book, The Intelligent Investor, which he later called “by far the best book about investing ever written.” In August 1950, Buffett applied to Columbia and wrote a persuasive letter. The letter found its way onto the desk of David Dodd, associate dean in charge of admissions. He accepted Buffett on the spot.

Columbia University Business School and Ben Graham

At Columbia, Buffett also read and almost memorized Security Analysis, written in 1934 by Graham and Dodd. To Buffett, Graham was a god and was surely the formative influence on Buffett’s investment philosophy. As it turned out, Ben Graham was also chairman of a little insurance company called GEICO. Wanting to learn more about GEICO, Buffett went to Washington, D.C. to visit the company. He met with GEICO’s financial vice president, Lorimer Davidson, who graciously spent several hours with Buffett, answering his questions about the company. When Buffett returned to New York, he sold 75% of his growing stock portfolio to buy 350 shares of GEICO. That’s how sure he was that GEICO would be a superb investment. The company was growing rapidly and trading at only eight times earnings. And, of course, learning about GEICO and how the insurance business works (and the value of “float”), primed him to invest not only in insurance stocks throughout his career, but led him later in his career when he was running Berkshire Hathaway to fully acquire GEICO in 1996.

Ben Graham, greatly influenced by the poor economy and difficult stock market during the Great Depression, thought that the best way to prosper in the stock market was to analyze a company’s balance sheet to determine its “intrinsic value.” He emphasized having a “margin of safety” when buying a stock. If a company’s stock was trading at a substantial discount to the cash that could be realized if properties and inventories were sold off and receivables collected and its debts repaid (i.e., its book value or net worth), the stock could likely be safely bought. In other words, the stock would be trading at a discount from its intrinsic value. Buffett would later write about this investment approach, calling it the “‘cigar butt’ approach to investing. A cigar butt found on the street that has only one puff left in it may not offer much of a smoke, but the ‘bargain purchase’ will make that puff all profit.”

Buffett’s Investment Performance (1957-1969)

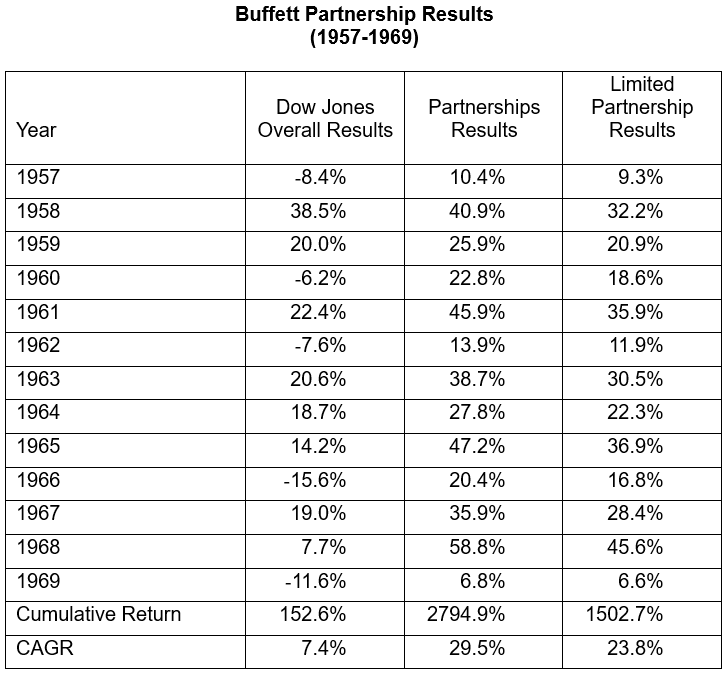

Buffett received his graduate degree from Columbia in 1951 and desperately wanted to work for Ben Graham’s investment company, Graham-Newman. He even offered to work for free. However, Graham turned Buffett down — at the time, Graham only hired Jewish employees to counter discrimination on Wall Street. Instead, Buffett returned to Omaha and worked as a stockbroker at the firm that his father had cofounded, Buffett-Falk. He worked there for three years until Graham agreed to hire him in 1954. Then in 1956, Buffett struck out on his own. He started with approximately $1 million under management in seven partnerships, and when he later merged the various partnerships into Buffett Partnership Ltd. in 1962, he had $7.2 million in client assets. The table below chronicles the investment performance of Buffett’s partnership.

The difference between the partnership results and the limited partnership results is due to the investment management fees paid to Buffett. When he shut down the partnership in 1969, there were 300 limited partners and total assets of over $105 million. $1,000 invested with Buffett in 1957 was worth over $27,000 when he dissolved the partnership at the end of 1969. He closed down the partnership because Ben Graham’s game was over — the market no longer presented ample opportunities to employ the cigar butt approach and was overvalued after a 17-year secular bull market starting in 1949.

Buffett’s partnerships never experienced a down year in this 13-year period, and the bulk of the profits in his partnerships were made using the Ben Graham balance sheet method — the cigar butt approach. During this period, Buffett would often sit at home in his bathrobe scouring the Moody’s Manual, seeking public companies whose balance sheets indicated that their stocks were trading for less than their intrinsic value, i.e., less than their net worth, and sometimes less than their cash on the balance sheet. Most of the companies in which he scored big were small cap companies — not on the radar screens of most investors. However, he made two major investments that were contrary to Ben Graham’s methodology — American Express and The Walt Disney Company. Buffett began to focus on these companies because of the influence of Charlie Munger, who had become a close friend in 1959. Munger maintained that Graham’s method only worked when practiced at a small scale. Munger encouraged Buffett to give up buying fair or poor businesses at wonderful prices, and instead, to purchase wonderful businesses at fair prices. And that’s what Buffett began to do.

The Purchase of Stock in American Express

Buffett’s purchase of American Express is a relatively well-known story, but it is well worth repeating here as it demonstrates several of Warren Buffett’s cardinal traits: his courage to buy the stock of a company when others were fleeing, and his willingness for a single investment to represent a very large percentage of his portfolio’s assets. The American Express story begins with how a major commodities trader, Anthony “Tino” De Angelis, used warehouse receipts for salad oil issued by an American Express subsidiary in Bayonne, NJ, to borrow large amounts of money from 51 banks. The American Express subsidiary stood as a guarantor of the quantity of oil in the tanks. A swindler at heart, De Angelis filled the tanks largely with saltwater, leaving just enough oil in the tanks to fool the auditors. When the price of soybean oil collapsed in 1963, the banks looked to the warehouse receipts as collateral for the loans and eventually found that their collateral was worthless. And of course, they looked to American Express to repay loans of more than $150 million. Initially, it wasn’t even clear if American Express would survive. But Amex was an emerging financial powerhouse — not only with its globally-recognized Travelers Cheques but also its American Express charge card, which was gaining market share at a phenomenal pace. If he had used his “cigar butt” method, he never would have bought Amex, because the real value of the company was its impeccable brand. Buffett didn’t just dive right in — being “greedy when others were fearful.” Instead, he carefully studied whether the salad oil scandal would harm its brand, damaging American Express irreparably. His investigations found that for clients, banks, and merchants, it was business as usual for the card and for the Travelers Cheques. Buffett began to purchase the stock carefully (in order not to drive up the price of the stock). And the stock was not a cigar butt, selling at 3 or 4 times earnings. Buffett began buying the stock at around $40 a share, when it was priced at a P/E of 14. But Buffett recognized its enormous growth potential and continued to buy the stock over the coming year — even as the claims would not be settled for years. By 1965, American Express was 33% of the partnership’s portfolio. It paid off enormously. Between 1964 and 1967, Buffett made $15 million off his $13 million investment, and American Express accounted for one-third of the partnership’s overall gains during this period. When he sold the stock, its P/E was over 30.

Buying Stock in The Walt Disney Company

In 1966, Buffett bought 5% of the outstanding stock in Disney for $4 million. Once again, Buffett did not follow the Ben Graham approach in making this investment. He did a great deal of due diligence before he made the purchase. He personally visited the company and met with Walt Disney. He went to Disneyland, built in 1955. “Mary Poppins,” released in 1965, was a huge hit globally, and he even went to a New York City movie theater to see it. The movie made $30 million that year — 37% of the market cap of the company in one movie. He decided to buy stock in Disney because of the timeless value of Disney films, as Disney had built an exceptional brand associated with high-quality, family-friendly films. Moreover, the company had transformed itself from a film company to an entertainment company. Following Charlie Munger’s advice, he bought a “wonderful company at a fair price.” Following the death of Walt Disney, he sold the stake in Disney about a year later with a 50% gain.

Buying Berkshire Hathaway

Employing his cigar butt strategy, Buffett started buying stock in this struggling textile company in New Bedford, MA in 1962. The saga of how Buffett gained a controlling interest in the company is beyond the scope of this commentary, but by 1969, Buffett owned 36% of it. In 1970, he became the company’s chairman and CEO. Essentially, buying Berkshire Hathaway was one of Buffett’s last efforts employing the cigar butt method. Charlie Munger called Buffett’s purchase “dumb.” Buffett himself described buying the Berkshire Hathaway textile company as the biggest investment mistake he had ever made. After struggling to make money in the textile business for almost 20 years, Buffett terminated all textile manufacturing in 1985. But turning a lemon into lemonade, Berkshire Hathaway became the holding company for all of Buffett’s operating and investment companies.

Katharine Graham and the Washington Post

Buffett had always been interested in the newspaper business and had over the years bought stock in various papers. In 1973, Berkshire Hathaway began to purchase shares in the Washington Post, accumulating a 10% position that year. The Post was managed by Katharine Graham, a famous hostess and doyenne in Washington, D.C. whose husband, Phil, had previously run the paper prior to taking his own life in 1963. Katharine was insecure in her role as publisher of the Washington Post and often sought the advice of the board members and other advisors. When she realized that Buffett was not seeking control of the Post, she brought him on the board in 1974. Soon he became her most trusted advisor. Buffett often stayed at her home when he was in Washington. In time, they developed a very intimate relationship — although all sources maintain that it was platonic.

Warren Buffett’s Unconventional Marital Life

Buffett’s sister, Bertie, introduced Susan Thompson, who grew up in Omaha and was her roommate at Northwestern, to Warren in 1950. Susie was mature, sophisticated, and generous with her emotions — all traits that Buffett lacked. He pursued her, unsuccessfully at first, but ultimately they were married in 1952, when Buffett was 22 years old. According to Buffett in Snowball, the marriage worked because Susie was a giving person, and Buffett, hampered by insecurities caused by his mother, was a needy person. Buffett, a genius in financial matters, was very much lacking in social graces, which Susie took care of in their marriage. However, as the years went by, Buffett’s investment prowess catapulted him into the big leagues nationally. He needed Susie less and less, and she developed other interests. In the 1970s, Buffett’s developing relationship with Katharine Graham seemed to trouble Susie, and she eventually decided to move to San Francisco, where she had an apartment. But Warren and Susie maintained their affection for each other. In fact, when Susie departed for the West Coast, she reportedly reached out to Astrid Menks, a waitress, and asked her to cook for Warren and look after him. In due course, Astrid moved into Buffett’s house and lived with him. They were now a trio, with Susie approving of the situation. Susan and Astrid apparently remained close friends. In fact, their joint Christmas cards were signed, “Warren, Susan, and Astrid.” So, in Buffett’s later years, Buffett maintained close relationships with three women, Susie, Astrid, and Katharine, all of whom apparently provided him with the support he needed in nonfinancial matters. We all have feet of clay.

Conclusion

Warren Buffett has become almost an American institution. Each year, 20,000 acolytes attend the Berkshire Hathaway Annual Meeting to drink in the wisdom of the Oracle of Omaha. Berkshire Hathaway owns approximately 80 operating subsidiaries. A large percentage of revenue from these subsidiaries comes from the insurance companies in the portfolio, the most well-known being GEICO. But Buffett also bought Burlington Northern and a large utility originally named MidAmerican Energy Holdings. When Buffett buys a company, part of the rationale behind his purchase is that he respects the management. Accordingly, he lets them run their businesses, which is one of the secrets of his success. Berkshire Hathaway also has an investment portfolio with positions in approximately 35 U.S. companies and nine foreign entities. His largest holdings by market value as of March 31, 2025, are Apple, American Express, Coca-Cola, Bank of America, Chevron, and Occidental, in that order. And now, with the current secular bull market lasting 16+ years and the stock market richly valued, Berkshire Hathaway is also shepherding around $350 billion in U.S. Treasury bills.

Warren Buffett, who will be retiring at the age of 95, is sui generis — one of a kind. A remarkable investor, although he, too, has made mistakes, such as his disastrous purchases of Dexter Shoe Co. and USAir preferred stock. And at times he has underperformed the S&P 500 benchmark for periods of five years or longer, the prime example being from 1995 to 1999 during the run-up to the internet bubble, when Berkshire Hathaway underperformed the S&P 500 by more than 75%. But Buffett’s long-term record is absolutely astounding. His IQ of 154 has clearly been a major factor in his success, but more important have been his key character traits — his patience, his discipline, his intellectual curiosity, his ability to gauge risk and to take the measure of people, and finally his courage to take large positions in stocks at the right time. All qualities that we as investors should seek to emulate.

Rob serves as chairman of Bradley, Foster & Sargent. He is a portfolio manager and member of the firm’s investment committee and its board of directors.

Rob founded Bradley, Foster & Sargent with Joseph D. Sargent and Timothy H. Foster. Earlier, he was president and CEO of Boston Private Bank & Trust Company, which he founded in 1985, and he spent 14 years with Citicorp, including 12 years in Europe, the Middle East, and Africa. Previously, he served as an officer in the U.S. Navy in Vietnam.

Rob served for seven years on the board of governors of the Investment Adviser Association, the national not-for-profit association founded in 1937 that exclusively represents the interests of federally registered investment advisory firms.

The Fog of War

Pei-ju Lee quoted in Quartz article on AI boom

Why Market Cap Matters for Diversification

One Big Beautiful Bill: A Summary

Turning Savings Into a Financial Plan

New Year, Same Goals? A Financial Check-In

Laying the Groundwork for Financial Freedom

A Look at Cybersecurity in a Changing World

How to Create Wealth in Your Retirement Accounts

Investing in 2024: Pros and Cons of Modern Strategies

Gold is Moving, Time for the Miners

Gold Ascending

A Cautious Look into the Future

Private Finance – Opacity Is Not a Virtue

Finding Your Tax Equilibrium

The Limits of Largesse

Demystifying Secure Act 2.0

A Suggestive Failure of Market Confidence

Fed Up?

Housing: A Little Too Frenzied?

Thoughts on Bitcoin and Cryptocurrencies

Gold: A Case of Excessive Pessimism

The Fed’s Freedom to Tighten is a Paper Tiger

ESG Epiphany

Investing with Keynes

Cash Flow Reigns King

Euthanasia of the Lender

Subscribe For More Articles On

Get the latest trends and thought leadership to help you make smarter financial decisions.