The $300-Billion Dollar Gamble: Can Hyperscalers Deliver on AI’s Promise?

Patience is a virtue – a saying we are perhaps all too familiar with. But on Wall Street it’s often the ultimate test of faith. True long-term conviction has become a rarity in a market increasingly dominated by high-frequency algorithms and an exploding options market. And yet, in the face of all that impatience, why are investors suddenly willing to wait for the AI payoff?

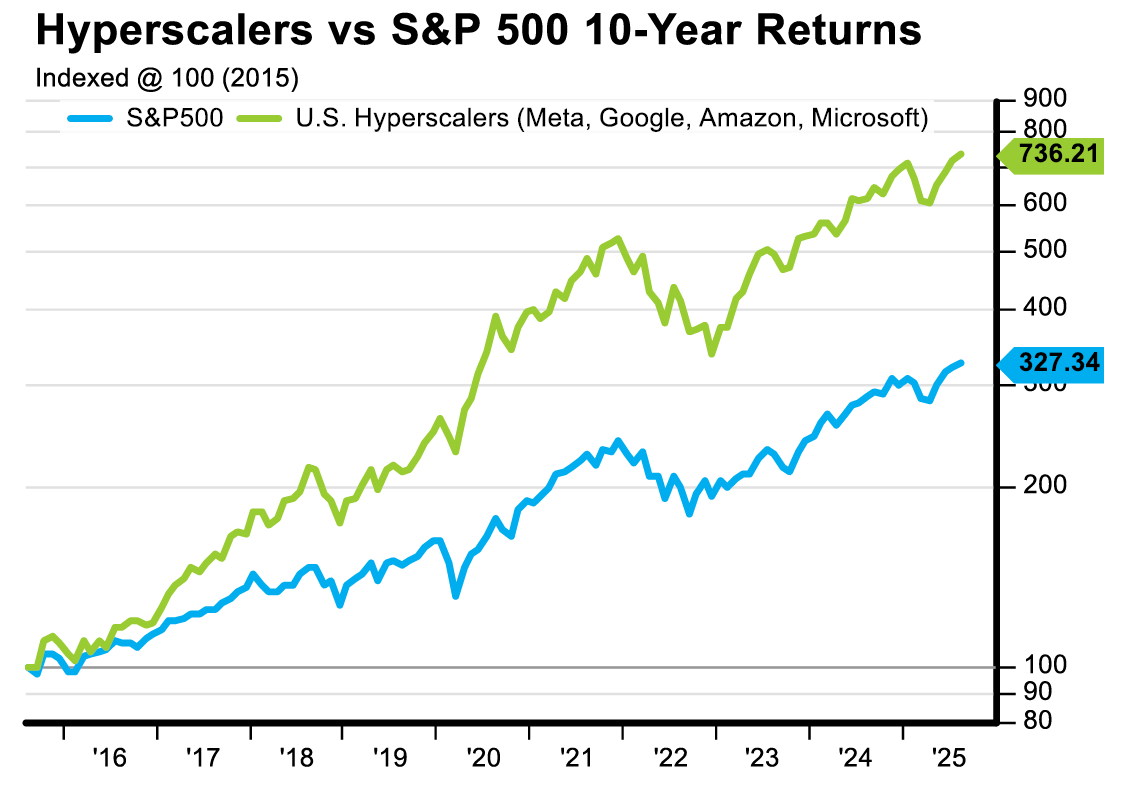

The post COVID-19 bull market for US equities has become heavily dependent on the success of AI implementation and the ultimate monetization of its models. For context, 70% of the S&P 500’s returns this year have been generated by AI-plays.

At the heart of this rally are the beloved hyperscaler’s (Meta, Microsoft, Alphabet, and Amazon) who are guiding a whopping $300B of capital expenditures related to AI advancements in 2025 alone. Following the Q2 earnings cycle, these companies have substantially accelerated their aggregate CAPEX forecasts – from an initial +20% YoY increase in January to a remarkable +45% today. Early 2026 guidance indicates no slowdown in this trend and leaves investors to wonder when the sales-to-capex inflection point will arrive.

Investing 101 teaches us that in order for a company to generate shareholder value in the long term, it requires them to make investments that sufficiently exceed their cost of acquiring capital. ROIC (return on invested capital) helps provide us with a tool to measure a company’s effectiveness in achieving this stated principle. So, when evaluating this recent spending spree, does this unusually high degree of patience seem justified– or are investors blindly betting on tomorrow?

Large capital expenditure cycles are not a new concept to the US equities markets, but the quality of today’s names offer limited comparisons through history.

Perhaps the most recent aggressive spending cycle was the Shale Era over a decade ago. Back then, drillers spent enormous amounts of capital to grow production rapidly ignoring the fact that the breakeven cost of new wells were depleting exponentially as technology improved. This eventually led to oversupply of oil, price declines, and diminished the ROI that made this discovery economically attractive in the first place. We often see many market participants attempting to draw parallels from this phenomenon to today’s spending behavior, but there are some important distinctions that make this inherently flawed.

Data between 1953 and 2023 reveals that often the highest quintile of YoY capital expenditures growth have underperformed the market in the years following. However the hyperscaler’s – for now at least – have seemingly broken this longstanding trend following strong outperformance in 2024 and the first half of 2025.

Why is that? – cash is king. Large-cap technology names have benefitted enormously from their prodigious free cash flow production. While the shale companies relied on external financing due to the businesses prolonged sales cycle, hyperscaler’s have the luxury of drawing on their legacy business to fund these expensive AI ambitions. Companies like Alphabet and Meta have core business segments (search, digital advertising) that feature robust margins and deep moats which help mitigate reliance on external financing. These shorter sales cycles provide these companies with immense cash flow to deploy at will and reward patience shareholders through buybacks and dividends.

As of the second quarter of 2025, the average free cash flow margins available to these hyperscalers sat at around 17%. This is a noticeable decline from 22.6% in 2023, but still comfortably above the general market which is in the realm of 10%. During this period, investors appear willing to accept declining free cash flows in hopes that the inflection point of accelerating sales growth is in the horizon and will compensate them appropriately.

Where is this “inflection point”, and how can these companies actually monetize AI technology?

Current analyst projections embed that CAPEX growth will fall behind sales in 2027, but the farther down the timeline you attempt to predict- the more uncertain it becomes. In a blue sky’s scenario, monetization evidence becomes material in the coming years, operating leverage can kick in, and free cash flow margins can return to historic highs for the hyperscalers.

Another promising development is the exponentially declining costs of inferencing in AI models, which is essentially the cost per query. This cost has declined by 95% since late 2022 and could potentially ease the capital intensity of these projects as data centers become more cost-effective.

Training – the cost to build the foundational model – on the other hand has been moving decisively in the opposite direction. ChatGPT 4 was nearly 20 times more expensive to train than ChatGPT 3, and recent data indicates that the cost to train a cutting-edge model has been increasing 2.5x every year! Recent AI research has discovered newfound training methods like knowledge distillation – seen in China’s DeepSeek model – which could help alleviate some of these cost pressures. However, investors have ample reason to question the hyperscale’s ability to capture the coveted prize of tangible ROI as the economics of the GenAI business remain largely uncertain.

How do we invest and approach this?

At Bradley Foster & Sargent, preservation of capital is of paramount importance to us. It should be in the investors’ best interest to be properly compensated for the respective level of risk they are willing to assume. All four hyperscale’s have proven to be consistent free cash flow juggernauts that present us with a reasonable margin of safety in the event that the AI monetization timeline becomes more prolonged than initially anticipated.

So far, 2025 has reaffirmed that patience is more than just a saying – it’s a principle that endures.

As an equity analyst, Colin is responsible for company, industry and stock analysis, in understanding competitive advantage, drivers of business, financial analysis, and valuation in order to develop robust recommendations in support of the firm’s investment of clients’ assets.

The Fog of War

People First. Then Technology

Pei-ju Lee quoted in Quartz article on AI boom

Why Market Cap Matters for Diversification

One Big Beautiful Bill: A Summary

Turning Savings Into a Financial Plan

New Year, Same Goals? A Financial Check-In

Laying the Groundwork for Financial Freedom

A Look at Cybersecurity in a Changing World

How to Create Wealth in Your Retirement Accounts

Investing in 2024: Pros and Cons of Modern Strategies

Gold is Moving, Time for the Miners

Gold Ascending

A Cautious Look into the Future

Private Finance – Opacity Is Not a Virtue

Finding Your Tax Equilibrium

The Limits of Largesse

Demystifying Secure Act 2.0

A Suggestive Failure of Market Confidence

Fed Up?

Housing: A Little Too Frenzied?

Thoughts on Bitcoin and Cryptocurrencies

Gold: A Case of Excessive Pessimism

The Fed’s Freedom to Tighten is a Paper Tiger

ESG Epiphany

Investing with Keynes

Cash Flow Reigns King

Euthanasia of the Lender

Subscribe For More Articles On

Get the latest trends and thought leadership to help you make smarter financial decisions.